Key Takeaways:

- Over $2 billion per quarter is being invested into InsurTechs in private markets

- The consumer sector has hoovered up ~70% of private market funding but the largest market cap public company today, Duck Creek ($5.7B), is B2B

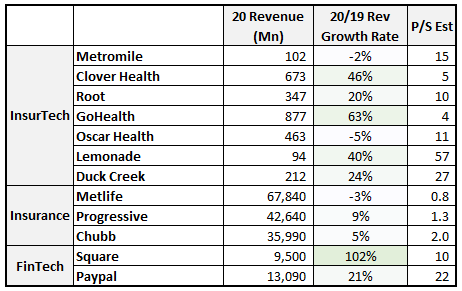

- GoHealth sports amongst the highest 2020 revenue ($877M) and revenue growth rates (63%) of the public InsurTechs

I have been enjoying watching the InsurTech market recently burst onto the scene. While I’m nothing more than an observer, here are some of my key findings on the space, so far.

Growing Market

InsurTech is elbowing its way into the zeitgeist. With the rise of public highflyers like Lemonade (LMND), Root (ROOT), metroMile (MILE), Oscar Health (OSCR), Clover Health (CLOV), Duck Creek (DCT), and GoHealth (GOCO), 2020 and 2021 have turned into a banner year for InsurTech IPOs and SPACs.

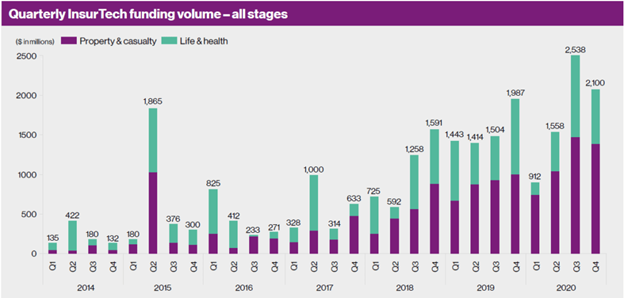

Not only public markets, in private markets, the deal volume and size continue to increase. The total funding amount in 2020 of $7.1B was 8x the amount in 2014, for an annualized growth rate of ~40%. Q3 and Q4 of 2020 were the two biggest quarters ever, each above $2b.

Source: CBInsights

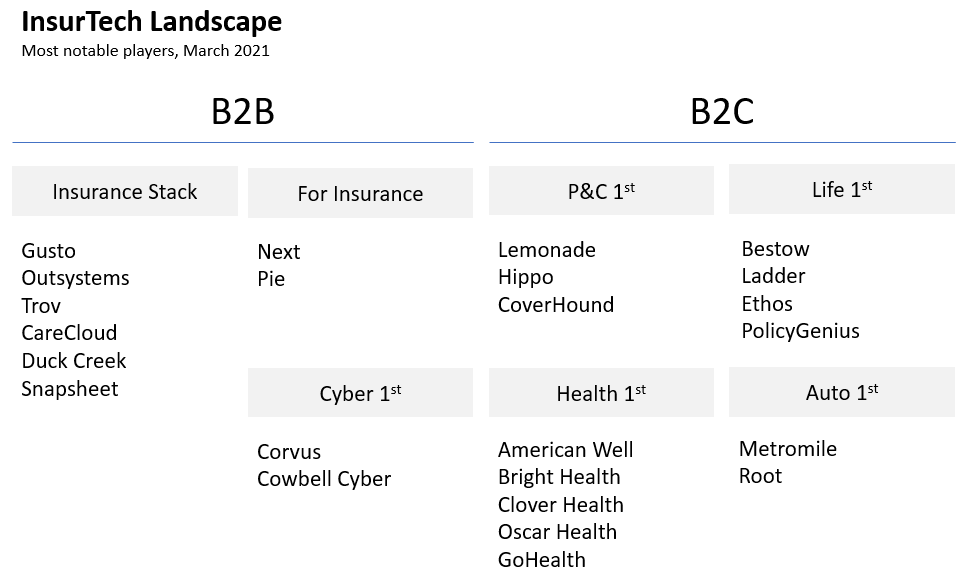

Landscape

With all the funding and attention, the landscape has developed significantly. In the chart above, CB Insights chose to categorize these players into two groups: Property & casualty, Life & health. That is a useful first-layer categorization. One thing it lacks is a distinction between B2B and B2C. Another thing it lacks is whether the insurer is, say, auto focused (a product type, like Metromile), or health focused (like Oscar).

As a result, what I have tried to do is categorize them by the type of insurance they are most known for, or the vertical which I believe is their largest business unit. PolicyGenius, for instance, operates in a few segments, but Life is understood to be its earliest and biggest segment. I have left out companies with small venture funding amounts that are nevertheless interesting (Lazarus, Relay, Halos, Spot, many more).

Source: Company websites; figure my own

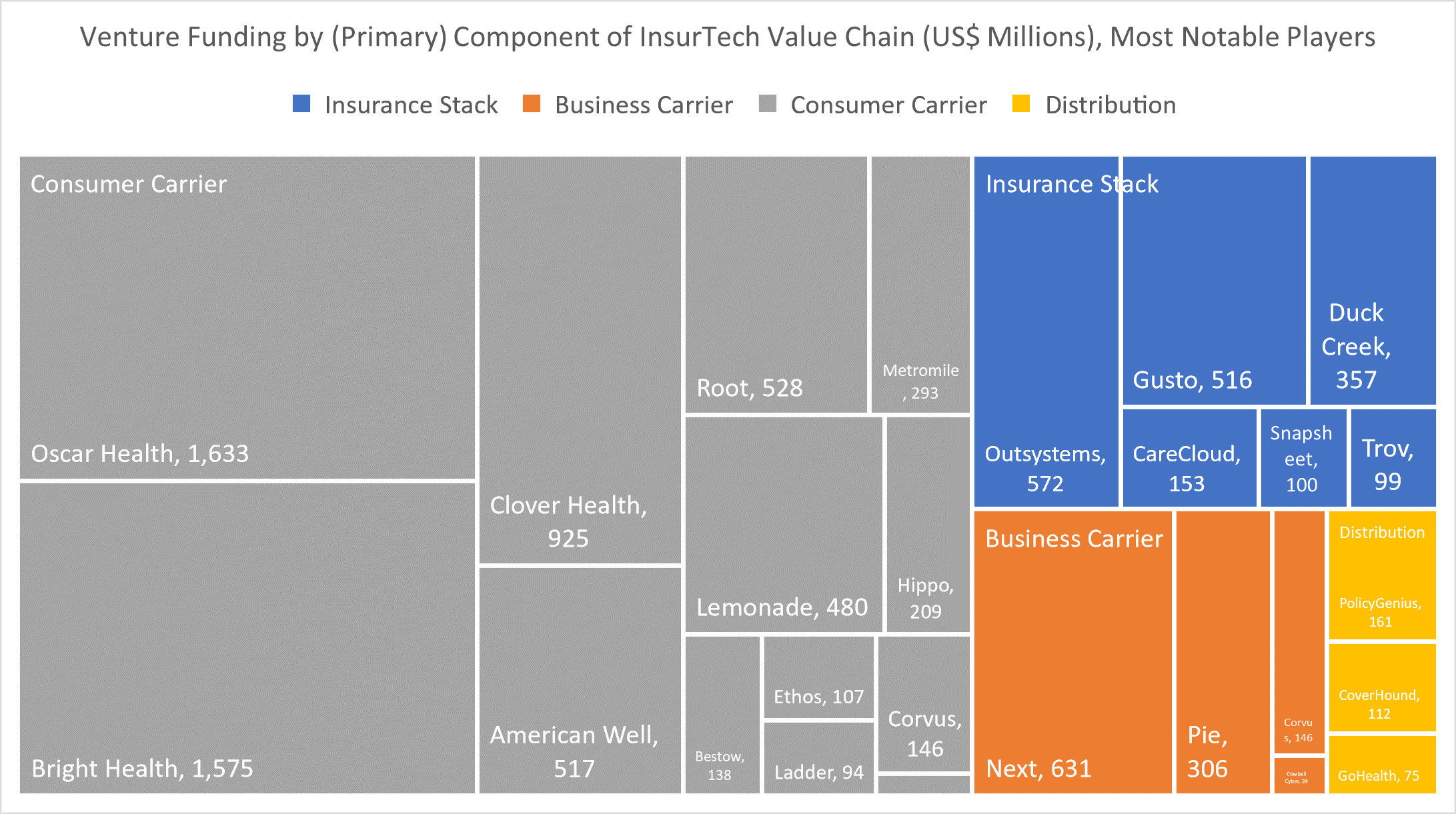

Continuing the PolicyGenius example, it is a managed marketplace, whereas Lemonade is a carrier itself. So, while the type of policy is one way to categorize these players, another is where they are focused on the value chain. Here I have visualized the top players by their total funding amount (another metric could be most recently estimated enterprise value, but less concrete and comparable across companies). This accounts for a total of $9.8B of funding into the space (certainly not all, but the biggest names I am aware of).

Source: Crunchbase; figure my own

Consumer Carriers have hoovered up much of the funding amount amongst these key players, ~71%. This includes consumer players across different focus areas, with the largest being health, which by itself is ~48%. These areas seem well-funded. As noted briefly, one distinction about this mapping vs the prior one I did above: while some P&C players like Lemonade from the above figure fall in Consumer Carrier in this figure, others like PolicyGenius fall in Distribution. They are not carriers themselves. Distribution represents ~3% of the funded amount.

The B2B side represents ~29% of funding dollars. Within that are the insurance stack players, which are ~18% of the total, and the business carriers at ~11% of the total. As usual, B2B seems smaller than B2C in highlighted company number and total funded amount but may end up being a larger part of public markets in the future (see cloud companies market cap vs consumer tech companies market cap). Duck Creek has the highest market cap of any of the public InsurTech players already.

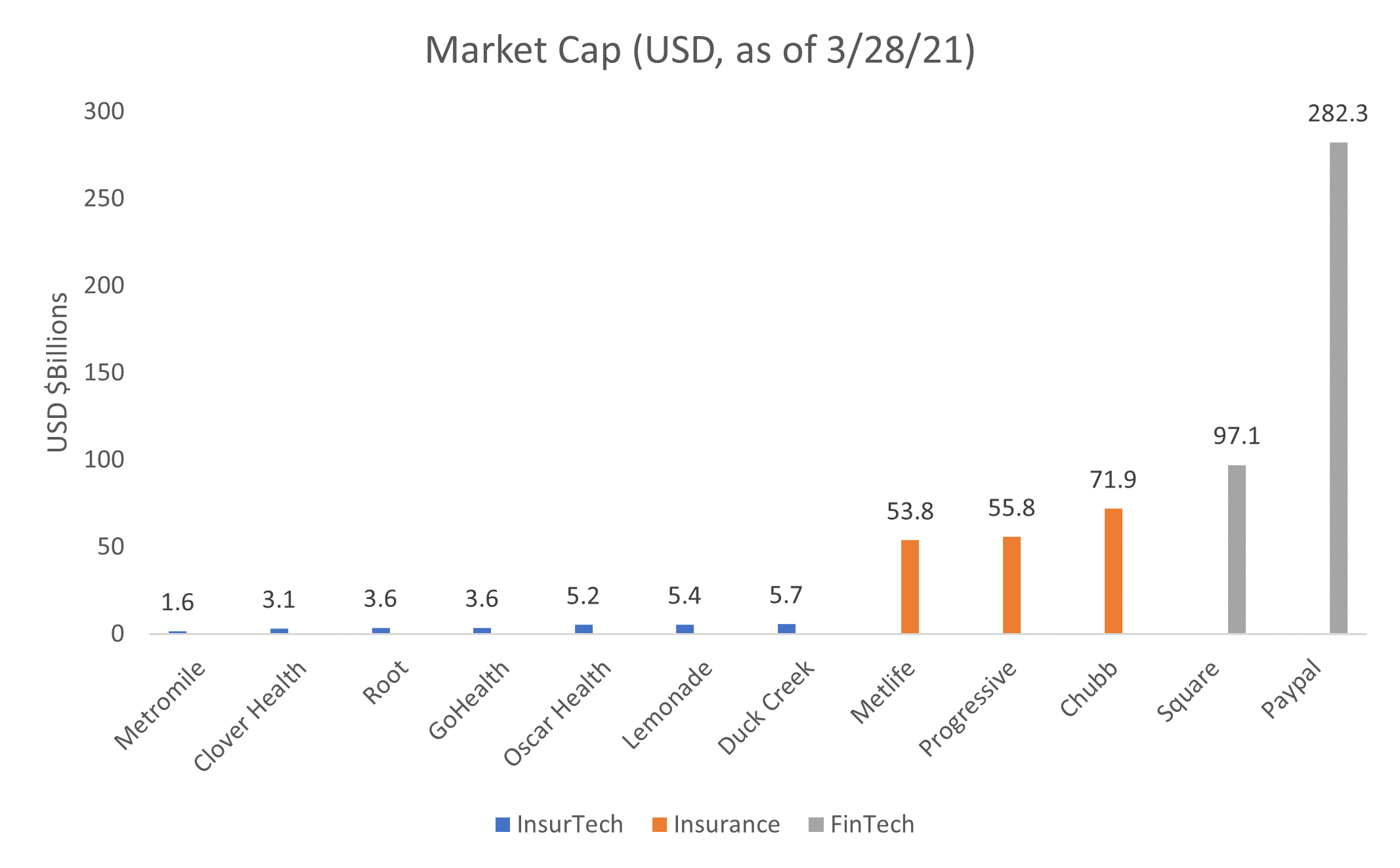

$100B+ Opportunity

It is about time. Like all the other corners of Finance where FinTechs are rising, Insurance has seemed ripe for disruption for ages. Most millennials and Gen Z’s still buy from the large, traditional carriers who offer subpar digital experiences. As a result, the InsurTechs are much smaller than FinTechs. Lemonade and Oscar have roughly~ $5B valuations, while FinTechs like Square and Paypal have ~$100B and ~$300B valuations. It seems likely that companies built for these digital first generations can succeed and grow into similar stratospheric market caps one day. It is not as if the Insurance marketplace cannot carry such a market cap. Chubb has a ~$70B valuation, while Progressive and Metlife have ~$55B valuations.

Source: Google stocks as of 3/28/21; figure my own

As these InsurTechs grow, it will be interesting to see who can capture the opportunity. While we do not have much information to go off now, one thing we can look at is the public companies’ revenues and growth rates. There are certainly no public InsurTechs growing at Square levels. The largest revenue and fastest revenue growth InsurTech, GoHealth, is about 9% the size of Square, yet still growing slower at 63%. So it is not clear if any particular player is on the road to eating away at the giants like Metlife, Progressive, and Chubb.

Source: Company IR pages, actuals for all except Metromile for which used estimates; figure my own

Summary

InsurTech is a rapidly growing market with several public players recently hitting the market. Activity in the private markets has also grown at a rapid pace, roughly 40%/year. While funding has focused on consumer health as the biggest component, it will be interesting to see which players eventually grow into high enterprise value behemoths.

What do you think – who is positioned to capture the large opportunity? Is there a player that flew under my radar?

Additional Reading

Technology and innovation in the insurance sector. OECD

Digital disruption in insurance: Cutting through the noise. McKinsey

InsurTech on the radar. Oliver Wyman

2 replies on “The InsurTech $100B+ Opportunity”

Nice write up! Root recently came up on my radar on a list tracking short interest. As of today, ROOT has a short interest of 41%: https://www.highshortinterest.com/

That’s really high short interest! I haven’t dug deep enough into ROOT specifically to have a buy/sell recommendation, but it seems like a basket of high short interest stocks has done pretty well recently :D.