“Thinking deeply about payments.” In 2008, this sounded like the job of companies like Visa and Mastercard.

But, in the end, the company that disrupted the merchant payment experience was a small upstart.

After being fired from Twitter in 2008, Jack Dorsey came back with a new company that was thinking deeply about payments.

From the earliest days, Jack framed the enterprise in terms of social interaction. Accepting card payments and the exchange of money facilitate poor social interactions. It was awkward for the merchant to key in your amount, you over your card, then sign a receipt, only for you to throw it away.

He saw an opportunity to redesign the payment experience to facilitate that interaction. And just a few years later, the Square reader was ubiquitous. That would have been enough for most companies: one star product that redefined a market.

But Square wasn’t just about merchant onboarding. Yes, that was the first product. But Square’s larger vision was still about improving that entire payment experience and social interaction.

As a result, Square would go on to launch not only an amazing product on the merchant side, but also a starrer on the consumer side with the Cash App in 2013. Starting from a market that had been dominated by PayPal since the early 2000s, peer to peer payments, Square has expanded Cash App into a banking replacement for the underserved.

Between the cash card, direct deposit, boosts, stocks, and bitcoin, it has become a replacement for your checking account and your brokerage. Of almost any company in the US today, Square with Cash App has done the most to onboard the underserved in the financial system.

So few companies actually launch two giant products. It’s a fascinating tale, with many lessons for product people. How did Square, now Block, launch not one but two enormously successful products? Let’s find out.

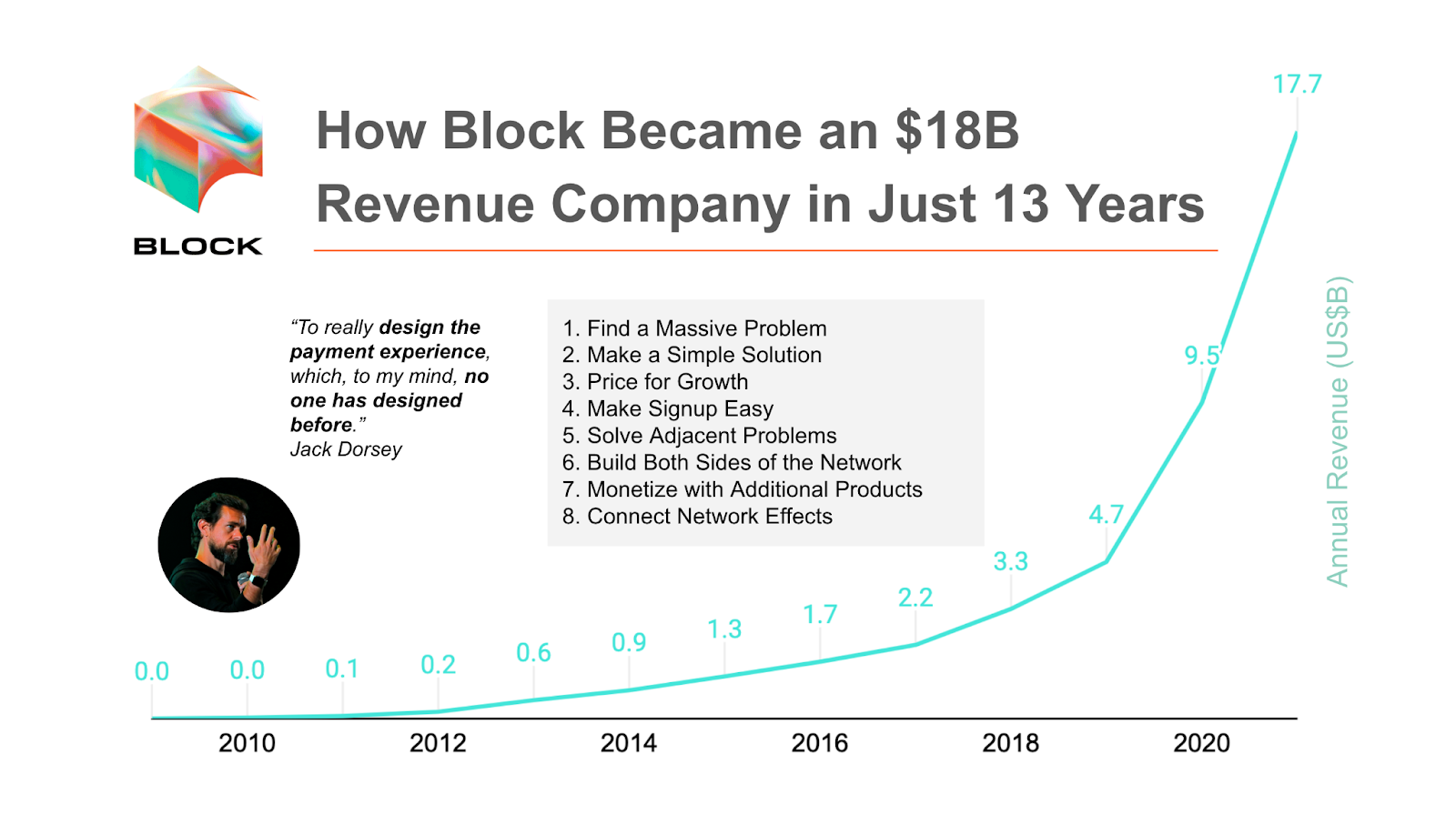

Lesson 1: Find a Massive Problem

2008

In 2008, Twitter fired Jack Dorsey. The site had grown rapidly since its 2006 founding. But frequent site crashes, allegations of poor management, and enmity between Jack and Twitter Chairman, Ev Williams, led the company to let go of its CEO.

Jack took it harshly.

It was like being punched in the stomach.

But he moved on quickly. The engineer turned CEO went back to his hometown, St. Louis, Missouri. He began chatting with several childhood friends about starting a new company.

One of those friends was Jim McKelvey. Jack had worked for Jim at a publishing software company back in high school.

Jim was a Jack believer. When Jack was 15, Jim hired him. Jack wasn’t like everyone else at the company. His acuity and work ethic was at another level. The next year Jim hired people in their 30s to work for Jack.

16 years later, Jim and Jack were on more equal footing. But Jim was no longer in tech. He was actually an artist living in the city.

One day, he had worked out a deal to sell $2,000 of his glass artwork. But the buyer did not have enough cash. Jim couldn’t accept credit cards, and the deal fell through.

Jim realized that it was too hard for small merchants like himself to accept credit cards. This was especially crazy given what else his iPhone could do: everything from surf the web to play music. He shared the problem with Jack. Jack agreed it was a huge problem.

The two dived into the world of payments to learn more. They quickly realized they could service the neglected micro segment of the market. There were over 15M merchants who also had that problem. It was a ubiquitous, severe problem.

The more they looked into the numbers, the more it validated the problem that small merchants were having trouble onboarding into payments.

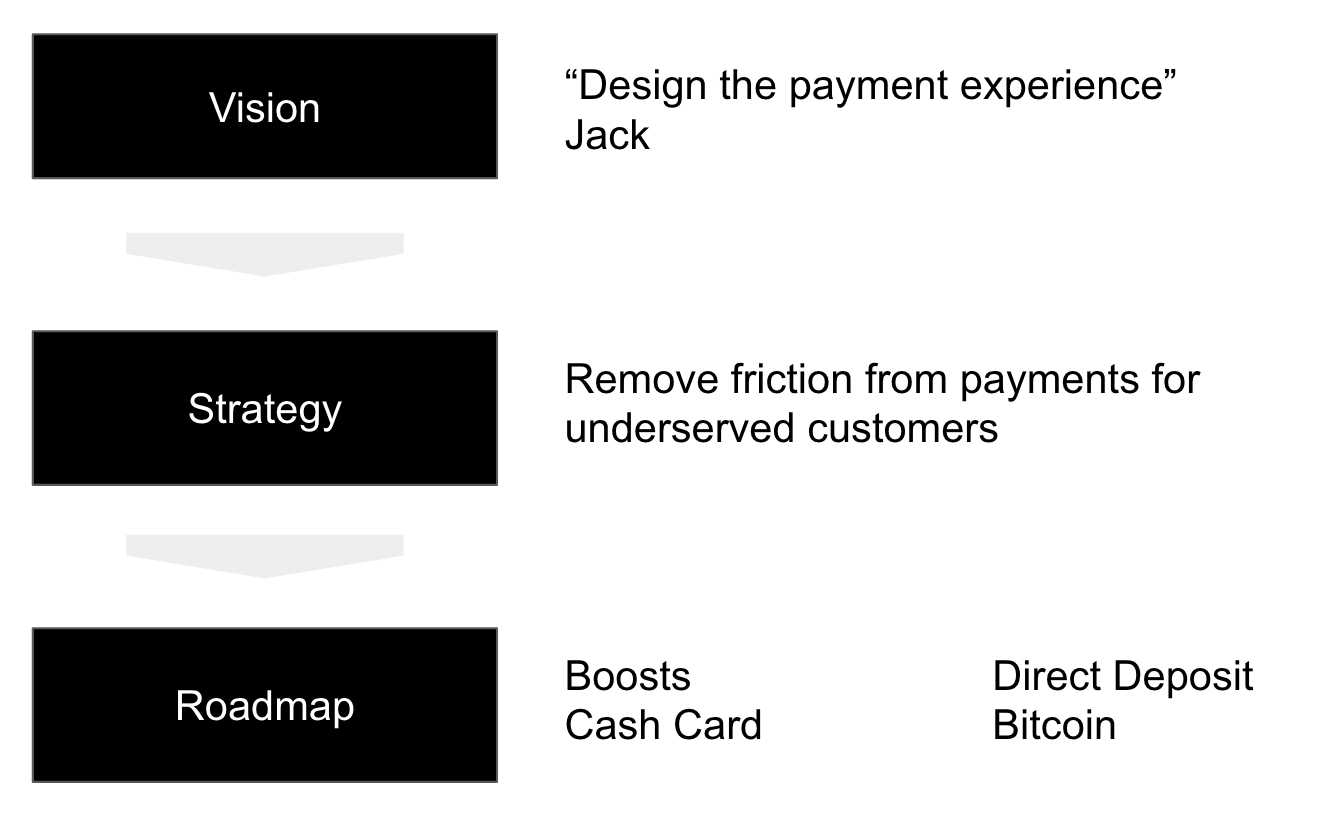

They got to tinkering with a solution in Jim’s home studio. They realized there was an opportunity to truly design the payment experience for merchant onboarding. As Jack said:

To really design the product experience, the payment experience, which, to my mind, no one has designed before.

Lesson 2: Make a Simple Solution

2009

In February of 2009, Square was born. Its mission: to enable anyone with a mobile device to accept card payments.

By the time Square was incorporated, Jim and Jack had created a prototype headphone dongle that would accept credit card payments. It was ingenious to design a solution with cheap components that could work through the headphone jack.

The duo went about iterating on their prototype and showing it to investors.

Naturally, investors loved it – and the opportunity to invest in the Twitter inventor’s next company. As a result, Square raised a “hyper-competitive” venture round valuing it at $40M before launching.

In a coup, the team also worked out agreements with Visa, Mastercard, and American Express to take Square payments. It was a complete card acceptance solution.

By the time Square officially launched, the first version of the product had instant product-market fit. Merchants loved that it just worked. Consumers loved that it accepted their existing payment methods.

Everyone loved that it was so beautiful. Today, the original dongle is featured in art museums.

Other companies noticed Square’s launch. But they still didn’t “get” it. When asked about Verifone’s competitor, Jack had this to say:

Square is not focused on allowing people who have merchant accounts to accept payments. It’s about allowing people to get in, immediately.

This inability for the established players to play Square’s game gave it a leg up for years to come. Square found a massive problem, onboarding people to accept payments immediately and freely, and design a simple solution that would drive its growth for years to come.

As Jack said on Charlie Rose, “It’s really complex to make something simple.” Square simplified the complex payment processing landscape for buyer and seller.

Lesson 3: Price for Growth

One of the most innovative aspects of the Square Reader was its pricing. Unlike the nearly $1000 machines merchants had to buy before Square, Square’s dongle was free.

Being $500 would have been cheap. $50 would have been mind-blowing. The Square reader was just completely free.

It was cheaper than cheap. As a result, Square effectively invented the concept of allowing micro-entrepreneurs to enter the credit card merchant economy.

Instead of a huge upfront dongle fee, Square charged 2.75% of the transaction. This was far lower than the 4% most processors charged small merchants.

It was especially cheap in light of the fact that Square gave the dongle away for free. Many of Square’s customers would just trial the dongle and never be profitable. Furthermore, of those who did try it, many would focus on small transactions where Square had to pay the card networks a per-transaction fee and actually lost money.

As a result of pricing for growth, Square had to keep its costs as low as its prices. There was no live support – no phone number to contact. As Jim McKelvey explained, this was actually beneficial. It forced Square to design innovations that removed the need for customers to reach out for support.

Pricing for growth also pushed the product team to have discipline in building solutions that didn’t need customer support. The interface was easy and elegant to use. It had few bugs or other causes for customer complaints.

One of the innovations to decrease customer complaints was fast settlement. Traditional credit card processors would pay customers after several days. Square built same-day settlement for most transactions, so merchants would get paid right away.

There was also no advertising or sales. For the first few years, Square grew squarely on the back of its innovations in merchant onboarding. Can you imagine a B2B company without a salesforce? That was Square.

2010

Of course, running a low cost business is not always smooth. As the Los Angeles Times put it, in 2010, the company “suffered from problems with its hardware and with credit processing and risk.”

So, it was perceived as a coup when the young Square landed PayPal veteran Keith Rabois to be the company’s COO. As Peter Thiel said at the time, “Any company that gets Keith will do extremely well.”

It actually, more or less, proved out. Keith helped address problems with hardware delays, as well as risk. He got nerdy about the risk and hardware problems. This helped Jack and the product teams focus on the core vision of designing the merchant signup experience.

Lesson 4: Make Signup Easy

Square designed the process of merchant signup. It followed through on Jack’s original vision. Signup was simple, easy, and intuitive.

The entire process could be completed online. There was no credit check or paperwork. You didn’t have to wait weeks for a decision either. The decision was instantaneous. Moreover, Square had no contracts. You didn’t have to read and sign a 40-page document.

Whereas every other processor was locking merchants into three-year contracts, Square customers could use the service as little or much as they wanted. Signup and use were 100x easier than the alternative.

2011 (~$100M)

All these innovations made Square’s growth meteoric. It grew 10% per week for its first two years. By the start of 2011, Square was processing close to a million dollars in gross merchandise value (GMV) a day.

On the back of those terrific numbers, the company raised another venture round. Led by Sequoia, it valued the company at $200M, at a time when few private companies reached such echelons. TechCrunch called it, “a Big Valuation.”

Just five months later, at the end of April, Square had doubled its GMV again, for $2M processed a day. The Square reader was a wonderful business that did an amazing job solving the problem of merchant payment onboarding.

Lesson 5: Solve Adjacent Problems

But the Square team wasn’t done there. Nearly as quickly as the company started up, it also began work on its second product. What it found in launching the reader was that customers had more needs than just a credit card processor. They needed to replace the cash register entirely. The entire credit card purchase experience was broken.

As a result, the company released Square Register in May. The Register app enabled iPads to replace cash registers as point of sale (POS) terminals. Square invented the now ubiquitous tablet terminals.

If the reader was about inventing the merchant onboarding experience, the register was about reinventing the credit card purchase experience.

As Jack explained, the Square register would set out to make credit card purchase easier for merchants and consumers.

Money is a concept that’s been with us for 5,000 years, and it’s never been designed to be anything but a burden. You come into my coffee store and order a cappuccino, and I hit the Cappuccino button on the cash register and see that it’s $3.24. And I take your credit card and type “$3.24″ into the credit card terminal. I swipe your card and give you the credit card receipt to sign. Then I take that back and staple it to the cash register receipt and give it back to you, along with your credit card. Then you take back the credit card and throw the receipts away. And meanwhile, at the end of the day, I have no idea how many cappuccinos I sold because it’s really difficult to access that information. It’s completely useless.

In that short “user story,” Jack outlines several adjacent pain points that the Register was designed to solve for the merchant:

- Inputting price information

- Using paper receipts for signatures

- Having data about what you sold

The register not only solved all three problems, it did so in a neatly designed package. Cash register attendants select items, not prices. Customers sign on the tablet. And merchants have clear data at the end of the day about what they sold.

Both reader and register fell under Square’s larger strategy of taking friction away from payments for small merchants.

Investors would validate these moves by Square with a massive $100M series C. While everything was growing gangbusters at Square, Twitter was not quite the same.

Three years after firing him, the company was under new management. Other co-founders Evan Williams and Biz Stone had left. Twitter CEO Dick Costolo asked Jack to take an operational role overseeing product, design, and brand. Jack decided to. He became Executive Chairman of Twitter, while staying as CEO at Square.

2012 ($203M revenue)

There was regular controversy about Jack’s two positions. But momentum continued steadfastly at both companies.

Twitter released a major redesign to be simpler. And as quickly as he stepped in, Jack stepped out. By October, 2012 he redirected his direct reports back to Dick.

Square, meanwhile, continued to invest in the consumer wallet experience. It struck up a deal for Starbucks to accept Square Wallet payments and process all other credit card payments. It was a major coup for the small company to be pairing up with such a large retail giant.

It also made the next big move in payment processing. Shifting away from the 2.75% transaction fee, the company announced a flat fee of $275 per month. This had the benefit of being more attractive to larger merchants, and helping Square with poor profitability for micro-merchants.

The company was rewarded for these moves, and ongoing momentum of its reader & register businesses, with a series D round that valued the company at nearly $3 billion.

By this point, the press was all over the Square story. Jack won awards like Innovator of the Year and was being written up in “leadership secrets” articles. He also delivered the keynote at Disrupt SF:

As he says in the talk, he considered Keith Rabois, COO of Square, a founder, because he had the attitude, and changed the course of the company.

2013 ($552M revenue)

Unfortunately for Square, Keith resigned in January. It was a messy situation, with Keith having a physical relationship with an employee who then accused him of sexual harassment. It was the type of moment that could have led astray a lesser company.

But Square endured to have another year launching terrific products. In fact, in 2013 the company would launch its second most important product: the Square Cash App. The P2P payments app allowed anyone with a debit card to send up to $2,500 a week for free.

Jack would also go from paper to actual billionaire, as Twitter would IPO to a 93% day-one pop. In a remarkable act of generosity for his Square employees, Jack gave back 10% of his shares. Today, they are worth $1.5B.

2014 ($850M revenue)

In 2014, Square kept making progress on Cash App. It added functionality so that you can request money to just a phone number over text, without the other end requiring the app. As always with a Jack Dorsey product, it was carefully designed. As Product Habits says:

Functionally, Cash wasn’t dissimilar to PayPal and emerging competitor Stripe. The key differentiator was that Cash felt much faster and was actually fun to use. Cash felt more like a social app, not a banking or finance app. This was a clever growth strategy

But not all products at Square have always worked. The focus of 2012, the Starbucks-Square Wallet partnership fizzled out. Starbucks stopped accepting Square Wallet for lack of volume, and Square sunset the project entirely.

Lesson 5B: Grow Products via Ecosystem

But it did make moves into three new markets. First, Square entered the food delivery market. It released a new app Order, and then acquired Caviar for $90M in stock.

Second, it also experimented with accepting Bitcoin transactions. In a case of “not wrong, but too early,” those efforts fizzled out.

Third, the company launched Square Capital. Square Capital offered small business loans that could be backed by the strong transaction data that Square already had about a merchant. This allowed Square to extend loans to businesses who previously could not access that capital.

These new products were establishing what has been called, “The Square Ecosystem.” Square was leveraging the great data generated by its payments & POS products to generate several other value added services for customers. These include financial services like Capital, analytics and employee management services associated with POS, and marketing services.

2015 ($1.27B revenue)

Things continued to go swimmingly at Square throughout the beginning of 2015. The company launched a new wireless version of the card readers that accepted the latest innovations in payments: chips and ApplePay. Square also redesigned the Cash App to be sleeker.

Twitter, on the other hand, needed Jack’s help again. So in October, Jack agreed to become permanent chief executive of Twitter (a role he would go on to hold for ~6 years). To quell anxieties at Square, he let employees know that he would not step down as chief executive until he was “old or dead.”

Pessimists thought that Jack’s dual-CEO roles might scuttle a Square IPO. The argument was investors would scoff at having half a CEO for the newly minted public company. But investors did not scoff.

After all, the Square Reader and Register “could feel ubiquitous at times,” by that point. Square had slowly been moving from small merchants making <$125K a year to a healthy mix of small and mid-size merchants.

In November 2015, Square IPO’d, with a 24% day one pop. That valued the company at just under $3 billion. It was a tough time for tech stocks, with durable companies like Hubspot and Etsy over 50% off their highs.

As a result, the IPO was disappointing for investors who had invested in the company three years earlier at that valuation. But it would turn out to be a steal. All those investors needed to do was hold. Since then, the company has over 20x’d its valuation. (At its peak valuation in February 2021, it had 50x’d).

2016 ($1.71B revenue)

Throughout 2016, Square continued to build its vast ecosystem of applications and services. It went international, to Australia and the UK.

Lesson 6: Build Both Sides of the Network

The product that really zoomed in 2016 at Square was the Cash App. The company shipped notable acquisition and monetization features.

For acquisition, the company released a virtual debit account by allowing features for customers to store funds in their square cash accounts. This was the first big shift from Cash as focused on payment processing to focused on pseudo-banking.

It led to an inflow of new underbanked customers. The underbanked is not an insignificant market. It’s roughly one quarter of US adults.

To monetize these new customers, the Cash App also began offering instant deposits on P2P transfers for a 1% fee. Previously, many transactions were processed the same day. But the company slowed those down to post the next business day to promote instant transfer monetization. It was classic price discrimination, to find out customers who were willing to pay for instant deposits.

In 2016, Square doubled down on not just build ecosystem around POS but also building an ecosystem around Cash App:

2017 ($2.21B revenue)

By 2017, Square’s core payments business was proving strong, and new businesses like direct deposit in the Cash App and Square Capital were also contributing to 25% of revenue. Things were doing well.

The company followed up the momentum on the consumer side with the launch of the Square Debit Card. This would prove an important product to continue to make Square services more sticky for consumers. After all, you carry your card on you.

In addition to the Card, Square also expanded into crypto. An early proponent of Bitcoin since 2014, Jack answered many interview questions about the hyperbolic rise of the cryptocurrency.

He felt it was the “future unlock,” for the company. For 2017, the focus was Cash App. The company added bitcoin trading for select users. Jack had actually participated in the company’s hackathon the year prior to help make it happen.

Square was making the move far beyond peer-to-peer payments for Cash App. As Jack explained:

We don’t consider this a peer-to-peer app and stop. We consider it much more and really around providing financial access to people

As Square continued to expand its product surface area with Cash App, it was really executing on Dorsey’s original vision of designing the payment experience from another angle.

Never one to slow down innovation, Square didn’t abandon the seller side of the business, either. It released new dedicated hardware. This helped the Square Register expand upmarket.

Although small sellers found the prior one screen display “clever,” the new two-screen display proved to be much easier for the cashier. There was no swivel required. Both merchant and consumer could act at once.

Notice Jack is now looking at a screen facing him instead of one he had flipped to show in the prior picture. The new terminal offered a smoother social experience. The company was continuing down the path of its original purpose to make the payment experience a better social moment.

Lesson 7: Monetize with Additional Products

2018 ($3.30B revenue)

In January 2018, Square announced Cash App would support bitcoin trading for all users.

This move has proven to be an ingenious one for the company to diversify the company’s business beyond payments. Just three years later, in 2021, Bitcoin would generate $10B of revenue for the company in a single year. Bitcoin has helped Square dramatically monetize Cash App.

Bitcoin trading also helped kick off download momentum that saw Cash App flirt in and out of the top 25 free apps. Throughout the year, Cash app would rank far ahead of competitors Venmo, Paypal, and Zelle.

It was a remarkable year of growth for Cash App. In addition to Bitcoin trading, another major launch was direct deposit in March.

This meant Square could accept paychecks. It was a game changer for growth, as users had an incentive to use Cash App if they didn’t have a bank account. It was a sustained differentiator from Venmo and PayPal for three years.

Between Cash Card, payments, and direct deposit wallet, Square could now offer most of the services of banks. All it was missing was cashing checks and wire transfers, relatively infrequent operations for many customers. This made the service quite attractive to underbanked communities.

The team followed up those launches with Boost in May. Boost is the name for Cash App’s loyalty program, where users can earn instant cash back boosts at select coffee and food chains. It proved to be a great driver of engagement for the Cash Card and Cash App.

2019 ($4.71B revenue)

With the success of direct deposit, Bitcoin, and Boost, Square doubled down on new financial products under the Cash App’s Super FinTech App umbrella. In 2019, it launched stock trading.

Stocks proved to be another hit to drive engagement and monetization of the user base.All these additional products add to the lifetime value of Cash App customers. This was critical for an app that had generated a huge network, but had yet to monetize dramatically.

In 2019, Cash App revenue more than doubled, as these products’ effects started to compound.

2020 ($9.50B revenue)

The momentum continued through 2020. Over the year, Cash App crossed $1B in gross profit. It had nearly become half of Seller’s gross profit, despite being a much younger business.

Lesson 8: Connect Network Effects

2021 ($17.66B revenue)

In 2021, Square would make its biggest acquisition ever. It acquired Afterpay for $29B all in stock. At 42 times trailing twelve month Afterpay sales, it was a hefty acquisition price.

But Square made the purchase to connect its two ecosystem’s network effects.

With the acquisition and Jack stepping down as CEO of Twitter to focus on Square, the company changed its name to Block. Today, Block has three main business lines:

- Square

- Cash App

- Afterpay

Afterpay is the glue between the Square and Cash App ecosystems. Afterpay’s growing consumer and merchant bases reinforce one another. Buy Now Pay Later (BNPL) companies like Afterpay integrate with merchants to appear on the checkout, which helps them get consumers. Then they create a compelling consumer marketplace of merchants to funnel them back.

Afterpay will be integrated into both sides of Square’s ecosystem. The bet is this will strengthen the connection between these ecosystems and help drive more commerce between merchants and consumers. Nowadays Square shareholder letters expressly begin with this new purpose:

We are focused on building software that creates differentiated, cohesive experiences between sellers and their customers.

The merchant-first company has become the payments and money company. To those who have followed Dorsey and Square from the beginning, this is no surprise.

Block also has a new business line it is trying to create all on its own: crypto. It has a variety of plays on crypto, from a dex to a hardware wallet. While none show material revenue today, they manifest Dorsey’s vision of reinventing money.

When thinking of how to reinvent money from the ground up, Dorsey has found that Bitcoin is the right design. As it results, he is one of the most prominent Bitcoin “maximalists” in the crypto ecosystem today.

Takeaways

Over the course of examining the history of Square’s incredible evolution into Block, we have learned 10 timeless product lessons.